Whoa there!

Looks like you’re getting a lot out of our resources — awesome! Want to get even more tailored insights that fit your specific needs? Let’s book a discovery call so we can help you achieve your goals faster.

.svg)

GLBA Compliance: A Step-by-step Guide

Get ready to turn GLBA compliance from a complex challenge into a manageable and successful part of your business strategy or your cybersecurity and compliance practice.

Understanding the ins and outs of the Gramm-Leach-Bliley Act (GLBA) is more than a regulatory necessity — it's a critical aspect of maintaining trust in the financial sector. In a world where data security challenges are constant, GLBA compliance is one of the best ways to uphold integrity and confidence in financial services.

Tackling GLBA demands a sophisticated and comprehensive approach. That’s why relying on spreadsheets for such a crucial process is like using a paper map in the age of GPS — outdated and inefficient.

In this guide, we'll explore the nitty-gritty of GLBA's requirements, who it applies to, and why it is so important, delve into streamlined approaches to achieving GLBA compliance, and cover how integrating GLBA into your business operations can be more than just a legal necessity — it can be a strategic advantage.

What is GLBA? A Comprehensive Overview

Enacted in 1999, the Gramm-Leach-Bliley Act (GLBA) – also referred to as the Financial Modernization Act of 1999 – is a pivotal U.S. law that transformed the landscape of financial information security and privacy. At its core, GLBA's mission is twofold: to allow financial institutions to merge and consolidate, while firmly establishing measures to protect consumers' personal financial information.

GLBA consists of two main pillars: the Financial Privacy Rule and the Safeguard Rule. The Financial Privacy Rule dictates how financial institutions must inform customers about their information-sharing practices and safeguard sensitive data, while the Safeguard Rule requires institutions to have a written information security plan, detailing how customer information is protected.

But GLBA isn't just a set of rules to follow. It's a commitment to maintaining the highest standard of privacy and security in the financial world. Compliance with GLBA means actively ensuring your organization securely stores customer data and uses it responsibly and ethically.

After announcing changes to the Safeguard Rule in 2021, the Federal Trade Commission (FTC) issued a final rule on privacy protections and required organizations to be compliant with all changes by June 9, 2023. Among the biggest changes is a new requirement that all relevant organizations implement an information security program aligned with the rule’s nine core elements.

Who Needs to Be Compliant with GLBA?

All financial institutions that access customers’ non-public personal information must be GLBA compliant. But don't let the term “financial institutions” mislead you into thinking it's just about banks and credit unions. In the eyes of GLBA, a financial institution is any business or entity that offers financial products or services. This includes (but is not limited to) banks, securities firms, insurance companies, and even car dealers. In Section 314.2(h) you can check if you’re covered.

But there's more. Third-party service providers working with these financial institutions are also required to be GLBA compliant. So if your business or client processes information or provides services that directly support financial activities, you should be GLBA compliant. The FTC considers you are “significantly engaged” in financial activities based on two key factors:

- Formal arrangements: For example, a retailer that offers consumers direct credit via a store credit card.

- Frequency of financial activities: For example, a business that regularly wires money to and from consumers.

You can a deeper dive into FTC-defined financial activities, here.

However, there are some GLBA exemptions as well as notice regulations. According to 12 CFR 216.1, the provisions do “not apply to information about companies or about individuals who obtain financial products or services for business, commercial, or agricultural purposes.” It goes on to clarify that these types of organizations are not considered financial institutions:

- Any person or entity involved in any financial activity subject to the Commodity Futures Trading Commission under the Commodity Exchange Act (7 U.S.C. 1 et seq.)

- The Federal Agricultural Mortgage Corporation or any entity chartered and operating under the Farm Credit Act of 1971 (12 U.S.C. 2001 et seq.)

- Institutions chartered by Congress specifically to engage in securitizations, secondary market sales (including sales of servicing rights), or similar transactions related to a transaction of a consumer, as long as such institutions do not sell or transfer non-public personal information to a non-affiliated third party.

Key Requirements of GLBA Compliance

To be in compliance with GLBA, you must meet standards and other requirements outlined in the Safeguard Rule, Privacy Rule, and Pretexting Provisions. Each of these sections has specific standards that must be met (or conditions that you cannot violate).

The Financial Privacy Rule: Your Customer’s Data, Their Rights

At the heart of GLBA is the Financial Privacy Rule. The rule requires financial institutions to provide each customer with a privacy notice, which must be a clear explanation of what personal financial information the institution collects, how it's shared, and most importantly, how it's protected. It's about ensuring customers have a transparent view of their data's journey.

All customers, regardless of your use of their non-public personal information (NPI), should get a privacy notice when you first establish your relationship (or if the customer agrees, within a reasonable time after it’s established). With some exceptions, if you share customer NPI with non-affiliated third parties, you must also provide:

- Opt-out notice if the customer doesn’t want you to share NPI

- Reasonable way to opt-out

- Reasonable amount of time to opt out before NPI disclosure

For consumers that you may share their NPI with non-affiliated third parties, they must also get a privacy notice and opt-out notice. For consumers that you don’t share NPI with non-affiliated third parties (or they’re exempt) you must:

- Explain that your privacy notice is available on request

- Explain how consumers can get a full privacy notice

- Include the opt-out notice

Every privacy notice is expected to include information about how your business collects, protects, and discloses NPI. The Privacy Rule requires all notices to include:

- Categories of information collected (example: NPI obtained from a consumer reporting agency)

- Categories of information disclosed (example: NPI provided on an application such as name, address, and phone number or account information)

- Categories of affiliates and non-affiliated third parties to whom you disclose NPI (example: insurance companies)

- Categories of information disclosed and to whom under the joint marketing/service provider exception

- When disclosing NPI to non-affiliated third parties under certain exceptions, a statement that the disclosures are made "as permitted by law."

- When disclosing NPI to non-affiliated third parties not within the exceptions, an explanation of consumers' and customers' rights to opt out of disclosures

- Any disclosures required by the Fair Credit Reporting Act

- Policies and practices to protect the confidentiality and security of NPI

The Privacy Rule does more than just explain what you should include, it also details how the notices should look, primarily that it must be “clear and conspicuous” on paper or your website. It must also:

- Be understandable

- Direct attention to the type and significance of the information

- Be easy to read

- Be distinctive

- If you put a notice on your website, it must go on a page consumers often use or on a page where they conduct transactions.

Finally, the Privacy Rule details how you should deliver your privacy notices. The notices must be in writing. They can be electronic, but only if your customer agrees. If you’re sending them electronically, the notice must be on your website and require receipt acknowledgment.

If your notices are not written or posted in your office, you’re considered non-compliant.

Opt-Out Notices

Opt-out notices must “clearly and conspicuously” describe your customers’ opt-out rights. It can be a part of your privacy notice or delivered to your customers when you give them your privacy notice.

The Safeguards Rule: Fortifying Data Security

Next up is the Safeguards Rule, the shield of GLBA. With the 2023 amendments to the Safeguard Rule, there now is a directive for all covered institutions to develop, implement, and maintain an information security program that includes administrative, technical, and physical safeguards.

The information security program is not prescriptive but must be “written and appropriate to the size and complexity of your business, the nature and scope of your activities, and the sensitivity of the information at issue.”

Under GLBA, every information security program should:

- Ensure security and confidentiality of customer information

- Protect against anticipated threats or hazards to the security or integrity of that information

- Protect against unauthorized access to that information that could result in substantial harm or inconvenience to any customer

The Pretexting Rule: Guarding Against Deception

Then there's the Pretexting Rule. Pretexting, the act of obtaining personal information under false pretenses, is a devious threat in the financial world. GLBA counters this by requiring institutions to put measures in place to prevent such deceptive practices.

Prohibition on Obtaining Customer Information by False Pretenses in Section 521 of GLBA says that financial organizations cannot make false, fictitious, or fraudulent statements or representations to a customer. Further, you cannot provide a document to an officer, employee, or agent of your business if you know that document may be forged, counterfeit, lost, stolen, fraudulently obtained, or if it has false, fictitious, or fraudulent statements or representations.

However, these standards have a few exemptions:

- When you’re testing your security procedures or systems to maintain customer NPI confidentiality

- If you’re investigating misconduct or neglect of an employee, officer, or agent

- If you’re recovering NPI that was obtained under false pretenses

The guidelines are also not applicable if a law enforcement agency is conducting official duties when an insurer is conducting an investigation into criminal activities, fraud, or misrepresentation, or related to collecting delinquent child support. They’re also not applicable if the information is reasonably available as a public record related to security laws.

Want to accelerate your GLBA compliance process?

With Apptega’s GLBA compliance software, you can use streamlined questionnaires, integrations to your sources of truth, and framework crosswalking to run through GLBA assessments and audits like a breeze.

The Definitive GLBA Compliance Checklist

Embarking on the path to GLBA compliance can feel like preparing for a marathon. You know the finish line — but that doesn’t guarantee it’s simple to get there. The key is in a well-structured checklist, a roadmap that guides you through your complete compliance journey.

- Understand Your Obligations

Your first task is to understand each section of the Act (Privacy, Safeguard, Pretexting) to clearly understand all requirements. Consider developing separate plans to ensure you’re achieving all three.

- See Where You’re Gapped with a Thorough Risk Assessment

Assess everything from data collection to disposal processes to uncover any risks that could impact the security, confidentiality, or integrity of customer NPI.

Either you or a third party can accelerate this process by leveraging compliance automation software like Apptega to easily breeze through simplified templates to assess compliance with the GLBA requirements and automate the collection of evidence.

A tool like this will also allow you to get real-time visibility and control of your GLBA compliance assessment process with intuitive reports and dashboards.

- Develop a Customized Information Security Program

Now, transform your risk assessment findings into an actionable plan. Your information security program should be as unique as your institution, addressing each identified risk with specific, measurable actions. This plan is your blueprint for safeguarding customer data.

- Implement Strong Data Encryption Practices

Secure NPI by implementing robust encryption for data in transit (as it moves) and at rest (when stored). This step is crucial in preventing unauthorized access and maintaining data integrity.

- Regularly Update and Test Security Protocols

Routinely evaluate and adjust your information security program to address GLBA compliance gaps. Consider working with third-party consultants and using compliance software to manage and evaluate program performance.

- Empower Your First Line of Defense

Your employees play a vital role in maintaining compliance. Regular, comprehensive training on GLBA requirements and data protection best practices is vital. Cultivate a culture where compliance is ingrained in every action and decision.

- Establish Clear Procedures for Detecting and Responding to Security Events

In the event of a breach or security incident, every second counts. Establish and rehearse clear, efficient procedures for detection, reporting, and responding to such events. This preparation can significantly mitigate potential damage.

- Run Regular Compliance Audits

Regular audits help ensure that your compliance measures are effective and up-to-date. Use these audits as opportunities to identify and rectify any gaps or shortcomings in your compliance strategy.

- Maintain Proper Documentation

Document every step of your compliance journey – from risk assessments to training logs, security plans, and audit results. This documentation is a narrative of your commitment to compliance and security.

- Stay Ahead of the Curve

The regulatory environment is dynamic. Keep abreast of changes and updates to GLBA regulations to ensure your compliance efforts are aligned with the current legal requirements.

Potential Penalties of GLBA Non-Compliance

If you’re a GLBA-covered entity, you can face penalties for non-compliance. While GLBA rulemaking is overseen by the Consumer Financial Protection Bureau (CFPB), the FTC enforces the Safeguard Rule and can take court action for Privacy Rule violations.

Other state and federal agencies may also play a role in GLBA enforcement and corrective actions. Through the FTC Act, the FTC can ultimately issue a cease and desist order for violations and in other instances can go to court to seek monetary relief for violations, which can include penalties.

In 2020, for example, the FTC announced it had reached a settlement with a mortgage analytics company that failed to make sure one of its third-party affiliates had secured personal data about mortgage holders. As a result, the company had to implement a comprehensive data security program, must undergo biannual security program assessments from an FTC-approved third party, and have a senior executive certify each year the company is complying with FTC guidelines.

Here are some of the key penalties and repercussions for failing to comply with GLBA:

Monetary fines for GLBA non-compliance can be substantial. Regulatory bodies can impose hefty fines per violation, which can accumulate rapidly, especially in cases of ongoing non-compliance or multiple infractions.

Beyond fines, non-compliance can lead to legal actions, including lawsuits from affected parties. These legal battles can be costly, time-consuming, and damaging to your institution’s reputation.

Perhaps the most lasting impact of non-compliance is reputational harm. In the financial sector, trust is paramount. Any breach of customer data or privacy can lead to a loss of confidence, affecting customer loyalty and potentially leading to a loss of business.

Non-compliance can also result in operational disruptions. Regulatory investigations and the need to rectify compliance issues can divert resources from normal business activities, impacting efficiency and productivity.

Falling afoul of GLBA compliance can put your organization under increased regulatory scrutiny. This heightened oversight can lead to more frequent audits and a prolonged period of close examination by regulatory bodies.

Finally — and perhaps most importantly — non-compliance can hinder your ability to seize new business opportunities. Partners and clients are more cautious in dealing with institutions that have a history of regulatory issues, limiting growth and expansion prospects.

Accelerating GLBA Compliance with Software

Meeting all the requirements for GLBA compliance is a complex process that requires continuous assessment and adaptation. That’s why leveraging the right tool (no, Excel isn’t the right tool) can be a game-changer. It can not only simplify the process and lower costs but also ensure thoroughness and accuracy. Here’s how specialized compliance software like Apptega can facilitate achieving and maintaining GLBA standards.

Apptega's Role in Simplifying GLBA Compliance

Apptega's cybersecurity and compliance platform offers a centralized hub for managing all aspects of GLBA compliance. With an intuitive interface and robust features, it transforms the often daunting task of compliance into a more manageable process as it provides instant insight with real-time scoring on how well you're meeting compliance requirements, where you may have gaps, and even offers recommendations on how you can move closer to your GLBA compliance goals.

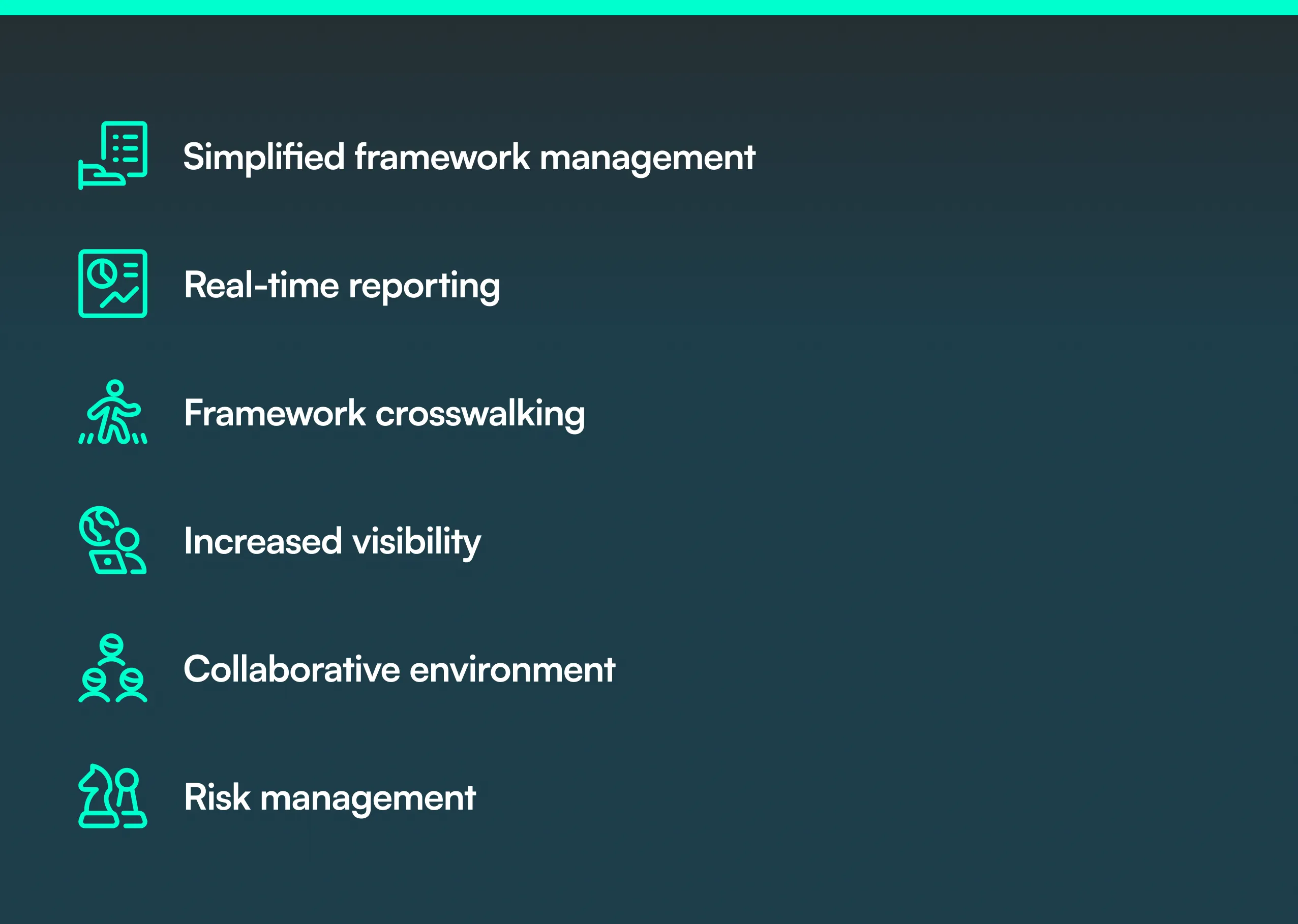

Here are the main aspects a tool like Apptega can help with:

Simplified framework management: With questionnaire-based templates covering all the controls and subcontrols of GLBA, running your risk assessments and identifying gaps becomes dead simple.

Real-time reporting: Get instant access to the data and information you need to report on your cybersecurity posture and compliance at any time.

Framework crosswalking: When you need to be compliant with more than one cybersecurity framework (GLBA + CCPA, for example) you can improve your program efficiencies by 50% or more by harmonizing controls across your frameworks using Apptega’s framework crosswalking feature.

Increased visibility: Demonstrate to your clients, key stakeholders, and the public that you are GLBA compliant with just a few clicks.

Collaborative environment: Facilitates collaboration among teams, making it easier to share information, assign tasks, and track progress.

Risk management: With Apptega’s Risk Manager tool, you can stack rank your risks and make sure you tackle the most pressing ones first.

For a detailed explanation of how you can use Apptega to consolidate the controls of GLBA and any other frameworks you need to comply with, watch this 4-minute demo video:

In short, software solutions like Apptega play a crucial role in simplifying and accelerating the GLBA compliance process. They provide a comprehensive, efficient, and user-friendly approach to managing the various facets of compliance, from initial assessment to ongoing monitoring and reporting.

GLBA Compliance FAQs

The opt-out notice requirement is reflected in Title V, Subtitle A of the Gramm-Leach-Bliley Act (GLBA).

GLBA’s purpose is to ensure financial institutions properly secure and manage private non-public personal information via its Safeguard Rule, Privacy Rule, and Pretexting Provisions.

No. There is not a GLBA certification, but you can work with a third-party auditor to confirm your GLBA compliance status.

If you’re required to be compliant for GLBA, it’s a good idea to have a third-party assess your compliance status. You can do this by working with a consultant or via software like Apptega, which can evaluate your compliance with real-time scoring.

The FTC has the authority to conduct official GLBA audits but, to ensure compliance before an FTC investigation, you can work with a third-party auditor to do a GLBA assessment for you.

There are many benefits of GLBA compliance. First, it’s a regulatory requirement, so you have to. Second, by complying with all GLBA standards, you can get insight into potential risks to all types of private and sensitive data in your environment, can make plans to address those risks and get insight into how effectively your existing controls protect and secure customer data. Compliance also will help decrease the likelihood of an NPI data breach, potential FTC investigation and audit, and hopefully lower your risk of facing penalties and other punitive actions.

Still have a question?

Get in touch with us and we would be happy to help.

Ready to get started?

Request a no-risk 14-day free trial to see how you can create a sticky compliance-as-a-service offering with Apptega.

Direct from the experts

Check out the latest news, resources and commentary from the Apptega team and a roster of veteran security and compliance professionals.

%20(20).png)